After years of meticulously tracking every dollar and paying off $50,000 in debt over three challenging years, I thought I had a pretty good handle on my personal finances. My budget was ironclad, my investments were automated, and my credit score was sparkling. Then, I dipped my toes into the exhilarating (and slightly terrifying) world of full-time gig work, and suddenly, a new financial beast emerged: quarterly estimated taxes. Let me tell you, it was a steep learning curve.

My journey from a W2 employee with predictable withholdings to a 1099 independent contractor responsible for my own taxes felt like switching from driving an automatic to a stick shift – exhilarating, but with a lot of potential for stalling out. This article is a deep dive into my personal experience, the mistakes I made, the lessons I learned, and the systems I built to conquer estimated taxes. I'm sharing specific numbers, real feelings, and the exact strategies I used, because I believe the best financial advice comes from those who've walked the path themselves.

Key Takeaways from My Estimated Tax Journey:

- Don't Underestimate: Always err on the side of overpaying slightly rather than underpaying. Penalties are no fun.

- Separate Savings: A dedicated, separate savings account for taxes is non-negotiable.

- Track Everything: Meticulous income and expense tracking is your best friend.

- Use the Right Tools: Software like QuickBooks Self-Employed and government portals like EFTPS simplify the process immensely.

- Proactive Learning: Don't wait for a penalty letter to understand the rules.

- It Gets Easier: The first year is the hardest. Once you have a system, it becomes routine.

Disclaimer: I am a personal finance writer, not a licensed tax professional or financial advisor. The information shared here is based on my personal experience and research, and it should not be considered tax advice. Tax laws are complex and subject to change. Please consult with a qualified tax professional for personalized advice regarding your specific financial situation.

The Uncharted Waters: My First Dive into Gig Work and Estimated Taxes

The year was 2021. I had just left my stable corporate job to pursue writing and consulting full-time. The freedom was intoxicating, the potential limitless. My first few months were a blur of landing clients through Upwork and direct outreach, setting up contracts, and generating invoices. Income started flowing in from various sources – Stripe for a client project, PayPal for a quick freelance gig, direct bank transfers for another. It was glorious, but also a little chaotic. My income in Q1 2021 alone jumped to around $12,500, a significant increase from what I had anticipated. This was a fantastic problem to have, but it also meant I was quickly blowing past the IRS threshold for estimated taxes.

My initial mindset, and this is a common misconception, was "I'll just deal with taxes at the end of the year, like always." I had always been a W2 employee, where my employer automatically withheld taxes from every paycheck. The concept of proactively calculating and sending money to the IRS four times a year was completely foreign to me. I knew about "self-employment tax" in theory, but the practical implications, especially the quarterly payment schedule, had not fully sunk in. I was so focused on generating income and delivering for clients that the administrative burden of taxes felt like a distant future problem.

Decoding the Beast: What Are Estimated Taxes, Anyway?

It wasn't until a casual conversation with a fellow freelancer that the gravity of the situation hit me. "Are you making your estimated payments?" she asked, with a knowing look. My blank stare was all the answer she needed. That evening, I dove headfirst into IRS Publication 505 and the labyrinthine pages of IRS.gov.

Here's the gist of what I learned:

- The "Pay-As-You-Go" Principle: The U.S. tax system operates on a pay-as-you-go basis. If you're a W2 employee, your employer handles this through payroll withholding. As a self-employed individual, you become your own employer, responsible for paying income tax, Social Security, and Medicare taxes (known collectively as self-employment tax) throughout the year as you earn income.

- Who Needs to Pay: Generally, if you expect to owe at least $1,000 in tax for the year from your self-employment income, you need to pay estimated taxes. This threshold is surprisingly easy to hit even with part-time gig work.

- The Schedule: These payments are typically due on April 15, June 15, September 15, and January 15 of the following year. If a due date falls on a weekend or holiday, it shifts to the next business day.

My biggest misconception here was thinking that because I wasn't earning a "salary," the rules were different. They aren't. Income is income, and the IRS wants its share, whether it comes from a paycheck or a PayPal transfer.

My First Year's Fumbles and Learnings (The Struggle is Real)

My first year of estimated taxes was a masterclass in what not to do. I made several missteps that cost me time, stress, and a bit of money. These were my primary struggles:

Mistake #1: Underestimating My Income (and Overestimating My Luck)

When it came time to calculate my Q1 (January 1 - March 31) estimated tax payment due April 15, 2021, I made a critical error. I looked at my projected income for the *entire year* and simply divided it by four. I was still new, so I predicted a conservative annual income of $40,000. This meant I estimated I'd owe about $2,500 in federal taxes for Q1 (roughly 25% of $10,000, assuming a 25% tax rate including self-employment taxes). I paid that $2,500 by the deadline, feeling vaguely responsible.

The problem? My actual Q1 income was closer to $12,500, thanks to a few unexpectedly lucrative projects. My self-employment income alone was around $11,000 after basic deductions. When I eventually reconciled my taxes, I realized I should have paid closer to $3,500 for that quarter. The initial confidence I felt quickly turned into a creeping dread as I started to understand the implications of underpayment.

Feeling: Initial naive confidence, followed by growing anxiety as the reality of my miscalculation set in.

Mistake #2: The Dreaded September 15th Deadline Miss

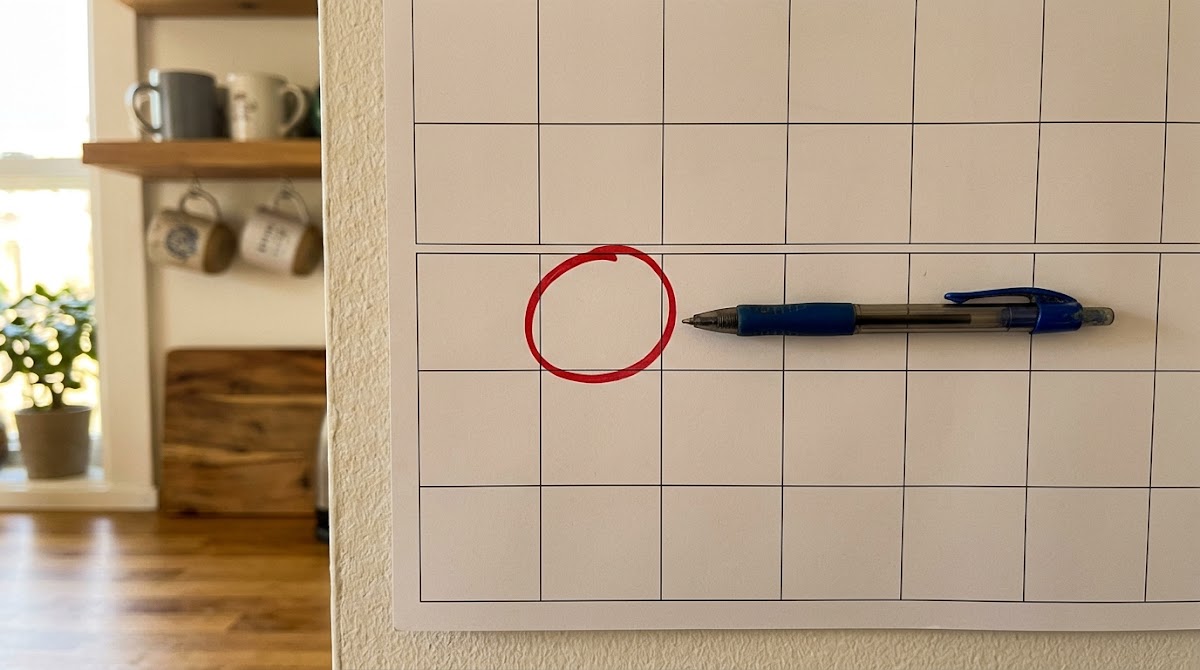

This was my biggest blunder, a moment of pure panic and self-reproach. The Q3 payment (income earned June 1 - August 31) was due on September 15, 2021. I had been diligently tracking my income with QuickBooks Self-Employed and had a good idea of what I owed. I even had the money set aside in my dedicated tax savings account. But life happened. I was deep in a major client project, traveling, and frankly, just overwhelmed. The deadline slipped my mind.

It wasn't until late October, when I sat down to review my financial calendar, that I saw it: the bright red circle around September 15th, mocking me. My stomach dropped. I immediately logged into EFTPS.gov (more on this invaluable tool later) and made the payment of $4,200 I should have made a month ago. I felt physically ill, knowing a penalty was likely heading my way.

Sure enough, a few months later, a letter with the dreaded IRS logo arrived. It was a CP14 notice, informing me of an underpayment penalty of $85. It wasn't a huge amount, but it was completely avoidable. I called the IRS helpline, explained my situation, hoping for leniency as a first-time freelancer. The rep, while polite, simply stated, "Sir, the due dates are published. We require timely payment." There was no wiggle room. I paid the penalty, a bitter pill to swallow, but a powerful lesson learned.

Feeling: Initial panic and self-reproach, followed by frustration and resignation when the penalty arrived. It felt like a direct consequence of my disorganization.

The Calculation Conundrum: General vs. Annualized Income Method

One of the most confusing aspects was how to actually calculate the quarterly payments, especially with fluctuating income. The IRS offers two main methods:

- The General Rule (Regular Installment Method): This assumes your income is earned evenly throughout the year. You estimate your total annual income, deductions, and credits, calculate your total tax, and divide it by four. This is what I initially tried, disastrously.

- The Annualized Income Method: This method is designed for those with significant income fluctuations. You calculate your income and deductions for each payment period (e.g., Jan 1 - Mar 31), estimate your tax for that period, and then "annualize" it to determine your payment.

My income was anything but even. Q1 was strong, Q2 was a bit slower as I focused on business development, and Q3 saw another surge. Initially, I tried to force my income into the general rule, which led to my Q1 underpayment. For Q2 and Q3, I started attempting the annualized method, which was complex with my spreadsheet setup. I found myself spending hours trying to project future earnings, which felt like staring into a crystal ball.

Here's a simplified comparison of how these methods *could* have impacted my Q1 payment, if I had understood them better:

| Calculation Method | Q1 Income Used | Estimated Annual Income | Estimated Q1 Tax Payment (approx. 25% rate) | Feeling |

|---|---|---|---|---|

| General Rule (My Mistake) | N/A (Projected evenly) | $40,000 | $2,500 | Overconfident, then anxious |

| Annualized Income Method (What I should have done) | $12,500 (Actual Q1) | $50,000 (Annualized from Q1) | $3,125 | More accurate, less stressful long-term |

Ultimately, I found a hybrid approach worked best for me: I used the annualized method to calculate my *current quarter's* liability based on actual earnings and expenses, but then I'd always add a small buffer (5-10%) on top, just in case. This became my personal "peace of mind" tax cushion.

Building My Estimated Tax System: Tools and Strategies That Actually Worked

After the initial chaos and the penalty letter, I knew I needed a robust system. I couldn't afford to be reactive; I had to be proactive. Here are the tools and strategies that became indispensable:

Dedicated Tax Savings Account: My Capital One 360 Performance Savings Setup

This was perhaps the single most impactful change I made. From the moment I received my first payment as a gig worker, I committed to setting aside a portion for taxes. I opened a separate Capital One 360 Performance Savings account and labeled it "Tax Savings." This high-yield savings account (HYSA) allowed me to earn a little interest on my tax money before it went to the IRS.

My rule: 30% of every payment I received went directly into that account. If I got a $1,000 payment from a client, $300 immediately moved to my tax savings. This percentage was based on an estimate of my combined federal income tax and self-employment tax bracket, plus a buffer. I started with 25%, but quickly bumped it to 30% and then 35% as my income grew and I wanted to be extra cautious. Seeing that balance grow gave me immense relief; I knew the money was there when the due date arrived.

Feeling: Immense relief and control. Seeing that separate balance grow was incredibly calming.

Tracking Every Penny: My Love Affair with QuickBooks Self-Employed

Meticulous record-keeping is non-negotiable for self-employed individuals. I initially tried to track everything in a Google Sheet, but it quickly became cumbersome. Then I discovered QuickBooks Self-Employed. This software was a game-changer.

- Bank Integration: It linked directly to my business bank accounts and credit cards, automatically importing transactions.

- Categorization: I could easily categorize income and expenses (e.g., "Advertising & Marketing," "Office Supplies," "Professional Development"). It even allowed me to set up rules for recurring transactions.

- Mileage Tracking: The mobile app automatically tracked my mileage, which was a significant deduction for client meetings and business errands.

- Estimated Tax Calculation: Crucially, it provided a real-time estimate of my quarterly tax liability, taking into account all my income and expenses. This made the annualized method much more manageable.

For example, in Q2 2022, I purchased a new laptop for $1,500 specifically for my business. I simply categorized it in QuickBooks, and the software automatically factored it into my deductions, reducing my estimated tax liability for that quarter by several hundred dollars. This direct impact on my tax bill, visible instantly, reinforced the importance of tracking every business expense.

Feeling: Empowered and organized. It transformed tax tracking from a chore into an automated, insightful process.

The Power of Proactive Payment: EFTPS.gov

After my September 15th fiasco, I vowed never to miss another deadline. The Electronic Federal Tax Payment System (EFTPS.gov) became my trusted ally. It's a free service provided by the U.S. Department of the Treasury that allows you to make federal tax payments electronically.

- Setup: The initial setup involves registering online and waiting for a PIN to be mailed to you, which takes about 5-7 business days. This is why you need to sign up *before* your first payment is due.

- Scheduling Payments: Once registered, I could easily schedule my quarterly payments in advance. I'd typically calculate my Q1 payment in late March and schedule it for April 10th, giving myself a buffer. For Q2, I'd schedule it in early June for the 10th, and so on. This meant I never had to worry about forgetting.

- Confirmation: You receive an immediate confirmation number, providing peace of mind.

I briefly considered mailing a check for my very first payment, but the thought of it getting lost or delayed filled me with dread. EFTPS is secure, reliable, and provides instant proof of payment. It's the only way I make my federal estimated tax payments now.

Feeling: Secure and confident. No more paper checks or last-minute scrambling.

The Numbers Game: How My Estimated Payments Evolved

Let's look at some real numbers from my first year and how my approach evolved:

-

Q1 2021 (Jan-Mar, Due April 15):

- Actual Gross Income: ~$12,500

- Initial Estimated Payment (based on $40k annual projection): $2,500

- Actual Owed (retrospectively calculated): ~$3,500

- Underpayment: ~$1,000

- Feeling: Frustration and a sense of being behind. This initial miscalculation set the stage for later stress.

-

Q2 2021 (Apr-May, Due June 15):

- Actual Gross Income: ~$8,000 (slower quarter)

- Calculated Payment (using QuickBooks SE, adjusting for Q1 underpayment): $2,800

- Feeling: Relief. I felt like I was starting to catch up and gain control. I specifically factored in a slightly higher payment to compensate for the Q1 shortfall.

-

Q3 2021 (Jun-Aug, Due Sep 15):

- Actual Gross Income: ~$14,000 (strong quarter)

- Calculated Payment (using QuickBooks SE, with 30% savings rule): $4,200

- Penalty for late payment: $85

- Feeling: Absolute dread when I realized I missed the deadline, followed by painful acceptance of the penalty.

-

Q4 2021 (Sep-Dec, Due Jan 15, 2022):

- Actual Gross Income: ~$16,000

- Calculated Payment (using QuickBooks SE, with 35% savings rule and buffer): $5,800

- Feeling: Pride and confidence. I had built my system, caught up, and felt prepared for tax season. By increasing my savings rate to 35% for this quarter, I ensured I had a healthy buffer.

By the time I filed my 2021 tax return in March 2022, I actually ended up with a small refund of $350, which was a pleasant surprise and confirmed that my aggressive catch-up strategy worked. The feeling of getting a refund, even a small one, after all that struggle, was incredibly validating.

Avoiding Estimated Tax Penalties: My Hard-Won Wisdom

The IRS imposes penalties for underpayment or late payment of estimated taxes. My $85 penalty was a stark reminder. Here's what I learned about avoiding them:

- The 90% Rule: You generally won't owe a penalty if you pay at least 90% of your current year's tax liability through estimated payments.

- The 100% (or 110%) Prior Year Rule: This is often the safest bet, especially in your first year of gig work. If your Adjusted Gross Income (AGI) in the prior year was $150,000 or less, you can avoid a penalty by paying 100% of your *prior year's* tax liability. If your prior year AGI was over $150,000, you need to pay 110%.

In my first year (2021), my prior year (2020) income was still W2, and my AGI was well under $150,000. So, I could have aimed to pay 100% of my 2020 tax liability. This would have given me a clear target number to hit throughout 2021, regardless of how much my gig income fluctuated. I wish I had known this rule and focused on it from day one. It offers a clear, tangible goal when your current year's income is unpredictable.

As NerdWallet aptly puts it, "The IRS doesn't want to wait until April 15 to get its money." They are serious about the pay-as-you-go system. If you do face a penalty, don't ignore it. Sometimes, you can request a waiver if the underpayment was due to unusual circumstances (like a disaster or disability), but simply forgetting usually isn't enough. My experience confirms this.

My Quarterly Tax Tips for New Independent Contractors

Based on my journey, here are my top tips for any new gig worker or freelancer facing estimated taxes:

- Open a Separate Tax Savings Account IMMEDIATELY: Seriously, do this before your first payment comes in. Transfer 25-35% of every payment you receive into it. This builds your tax war chest and separates it from your operating funds.

- Track Income and Expenses Meticulously from Day One: Use accounting software like QuickBooks Self-Employed, FreshBooks, or even a detailed spreadsheet. Categorize everything. Every legitimate business expense reduces your taxable income.

- Understand the 100% Prior Year Rule: This is your safety net. Calculate 100% (or 110%) of your previous year's total tax liability and aim to pay that amount in four equal installments. This guarantees you won't face an underpayment penalty, even if your current year's income explodes.

- Don't Be Afraid to Overpay (Slightly): A small overpayment means a small refund or credit next year. A small underpayment means penalties and stress. I always build in a 5-10% buffer now.

- Register for EFTPS.gov: Do this early! It takes time to get your PIN, but it's the easiest, most reliable way to make federal payments. Schedule your payments well in advance of the deadline.

- Set Calendar Reminders: Beyond EFTPS, I have recurring reminders in my digital calendar for each payment due date, set a week in advance.

- Consult a Tax Professional: Especially in your first year, consider hiring a Certified Public Accountant (CPA) or Enrolled Agent (EA). They can help you set up your system, understand deductions, and ensure you're compliant. I hired a local CPA for my first annual filing, and their guidance was invaluable.

- Keep Up with Deductions: Don't forget legitimate business deductions like home office expenses, business mileage, health insurance premiums (if self-employed), professional development, and software subscriptions. These significantly reduce your taxable income.

My first year as a self-employed individual was a whirlwind of learning, especially when it came to estimated taxes. What started as a source of immense stress and a costly penalty ultimately transformed into a streamlined, predictable process. By implementing dedicated tools and strategies, and learning from my mistakes, I now approach quarterly tax deadlines with confidence, rather than dread. If I can do it, you can too.

FAQ: Your Quarterly Estimated Tax Questions Answered

Q1: What if I don't make enough money to pay estimated taxes?

A: Generally, you only need to pay estimated taxes if you expect to owe at least $1,000 in tax for the year. This threshold includes both income tax and self-employment tax. If your net earnings from self-employment are less than about $400, you won't owe self-employment tax, but you might still owe income tax if you have other income. Always check the IRS guidelines or consult a tax professional if you're unsure.

Q2: My income fluctuates wildly. How do I accurately estimate my payments?

A: This is a common challenge for gig workers. The Annualized Income Method (using Form 2210, Underpayment of Estimated Tax by Individuals, Estates, and Trusts) is designed for this. It allows you to calculate your payment based on your actual income and deductions for each specific payment period, rather than assuming an even income stream throughout the year. Software like QuickBooks Self-Employed can help automate these calculations. Alternatively, use the 100% (or 110%) prior year rule as a safe harbor if your previous year's income was more stable.

Q3: Can I just pay all my taxes at the end of the year instead of quarterly?

A: While you *can* pay all your taxes at year-end, it's highly likely you'll incur an underpayment penalty from the IRS. The U.S. tax system is "pay-as-you-go." If you don't pay taxes throughout the year as you earn income, the IRS considers you to have underpaid for each quarter you missed. This is a common misconception that can lead to unexpected penalties.

Q4: How do I actually make the quarterly estimated tax payments?

A: The easiest and most recommended method for federal taxes is through the Electronic Federal Tax Payment System (EFTPS.gov). You can also pay by direct debit through IRS Direct Pay, by credit/debit card through approved third-party processors (which usually charge a fee), or by mail with Form 1040-ES payment vouchers. I personally use and highly recommend EFTPS for its convenience and ability to schedule payments in advance.

Q5: What happens if I overpay my estimated taxes?

A: If you overpay, the IRS will typically issue you a refund when you file your annual tax return. Alternatively, you can elect to have the overpayment applied as a credit towards your next year's tax liability. I prefer to err on the side of overpaying slightly to avoid penalties, knowing I'll get the money back or use it for future taxes.

Q6: Do I need to pay state estimated taxes too?

A: Yes, if your state has an income tax, you will likely need to make estimated tax payments to your state tax authority as well. The rules and thresholds vary significantly by state. For instance, in my home state of California, the Franchise Tax Board (FTB) has its own estimated tax payment schedule and forms (Form 540-ES). Always check your specific state's Department of Revenue or equivalent agency for their requirements.

Q7: What kinds of deductions can I take as a gig worker?

A: As a self-employed individual, you can deduct many ordinary and necessary business expenses. Common deductions include: health insurance premiums (if you pay them yourself), home office expenses, business mileage, professional development/education, business insurance, accounting and legal fees, advertising, supplies, software subscriptions, phone and internet expenses, and a portion of your self-employment taxes. Keeping meticulous records of these expenses is key to maximizing your deductions.

Sources

- Internal Revenue Service (IRS). Estimated Taxes. IRS.gov. Accessed [Current Date].

- Internal Revenue Service (IRS). Publication 505, Tax Withholding and Estimated Tax. IRS.gov. Accessed [Current Date].

- NerdWallet. Estimated Taxes: How to Pay If You're Self-Employed. NerdWallet.com. Accessed [Current Date].

- Investopedia. How to Pay Estimated Taxes If You're Self-Employed. Investopedia.com. Accessed [Current Date].

- Electronic Federal Tax Payment System (EFTPS). EFTPS.gov. Accessed [Current Date].

Written by Alex Chen. a personal finance writer at WealthSure Lab who paid off $50,000 in debt over 3 years and tracks every dollar of my portfolio.